What Is a Good Annual Limit for Pet Insurance?

A single ACL surgery can cost $6,000 in 2026, which can quickly exceed a $5,000 annual limit before recovery is even complete. This is why your annual reimbursement cap matters so much in pet insurance.

The real value of coverage depends not just on the limit itself, but on how it works with your deductible and reimbursement rate when major veterinary costs occur.

- $10,000+ annual limit is recommended, higher for high-risk pets.

- Payout depends on limit, deductible, and reimbursement rate.

- No rollover, and limits usually can’t be raised after diagnosis.

How Pet Insurance Limits Work

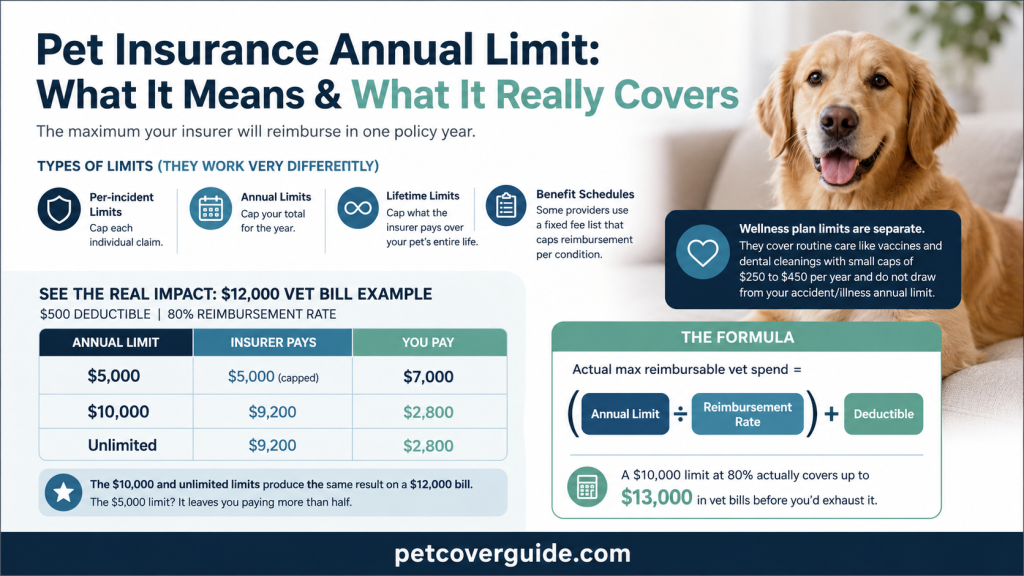

Your pet insurance annual limit is the maximum your insurer will reimburse in one policy year.

Once you hit that cap, you’re on your own until the policy resets. Simple enough on the surface, but there are several types of limits, and they work very differently.

Per-incident limits cap each individual claim. Annual limits cap your total for the year. Lifetime limits cap what the insurer pays over your pet’s entire life.

Some providers, like Nationwide Pet Insurance with its Major Medical plan, use a benefit schedule that caps reimbursement per condition using a fixed fee list.

Payouts under those plans can land well below the stated maximum. If you’re curious about how dental care fits into these structures, see how dental coverage is handled by most insurers.

Wellness plan limits are a separate category entirely.

They cover routine care like vaccines and dental cleanings with small caps of $250 to $450 per year. They don’t draw from your accident/illness annual limit.

Here’s the math most buyers miss. Your pet insurance annual limit doesn’t equal your payout. The deductible reduces the reimbursable amount first, and then the reimbursement rate kicks in.

Look at how the same $12,000 vet bill plays out across three limit tiers with a $500 deductible and 80% reimbursement rate:

| Annual Limit | Insurer Pays | You Pay |

|---|---|---|

| $5,000 | $5,000 (capped) | $7,000 |

| $10,000 | $9,200 | $2,800 |

| Unlimited | $9,200 | $2,800 |

The formula:

Actual max reimbursable vet spend = (Annual Limit ÷ Reimbursement Rate) + Deductible

A $10,000 limit at 80% actually covers up to $13,000 in vet bills before you’d exhaust it.

That means the $10,000 and unlimited limits produce the same result on a $12,000 bill. The $5,000 limit? It leaves you paying more than half.

What’s the Best Annual Limit

Use the “one-surgery test.” If a single major incident would exhaust your cap, it’s too low. Here’s what common conditions cost at the vet in 2026:

- TPLO surgery (torn ACL): $4,000 to $6,000 per knee

- Cancer treatment: $3,980 to $5,351 on average

- Bloat/GDV emergency surgery: $3,000 to $7,500

- Foreign body removal: $2,000 to $5,000

A $5,000 annual limit is effectively one-incident coverage. One torn ACL and you’re done for the year.

The best annual limit for pet insurance should absorb at least two major incidents, making $10,000 the practical floor.

BREED EFFECT

Breed matters a lot here. Large-breed dogs like Golden Retrievers, German Shepherds, and Labs face high orthopedic and cancer risks. They should carry $20,000 or unlimited coverage.

Small dogs and indoor cats are often well-served at $10,000 to $15,000.

Older pets of any size benefit from higher limits because claim frequency goes up with age.

If you’re unsure whether the cost is justified, you can see a full analysis of whether pet insurance pays off in 2026.

Pet Insurance Annual Limits by Provider

Not every provider offers the same annual limit options. Some only sell unlimited plans. Others give you a wide range of tiers.

Here’s how the major pet insurance providers compare on annual limits in 2026:

| Provider | Available Annual Limit Tiers | Unlimited Option | Notable Details |

|---|---|---|---|

| Trupanion | Unlimited only | Yes | Per-condition lifetime deductible; no annual deductible |

| Healthy Paws | Unlimited only | Yes | No limit tiers to choose from |

| Pets Best | $5K, $10K, $15K+, Unlimited | Yes | One of few with unlimited as an add-on tier |

| Embrace | $5K to $30K | No | Diminishing deductible rewards claim-free years |

| ASPCA Pet Insurance | $5K, $10K, Unlimited | Yes | Mid-range pricing with flexible tiers |

| Nationwide Pet Insurance | Varies by plan | Whole Pet only | Major Medical uses per-condition benefit schedule |

| MetLife Pet Insurance | $500 to $25K (in $1K increments) | No | Popular employer-benefit provider |

| AKC Pet Insurance | Tiered options | Yes | Underwritten by Independence American |

| Spot Pet Insurance | $2.5K to Unlimited | Yes | Wide range of customization |

| Lemonade Pet Insurance | $5K to $100K | No | Fast digital claims process |

Trupanion stands out with its unique model. You pay a per-condition lifetime deductible once, and then the plan covers that condition for life with no annual cap

Healthy Paws keeps it simple with no annual limit pet insurance as the only option.

The premium impact of choosing a higher limit is smaller than most people expect. Upgrading from $5,000 to unlimited typically adds 20% to 40% to your monthly premium. That’s often just $10 to $30 per month.

Compare quotes at $10,000 and unlimited to see the actual dollar gap for your pet. Our full breakdown of pet insurance pricing in 2026 shows how different tiers affect what you’ll pay for coverage.

What Happens When You Hit Limit

Once your annual limit is used up, you pay 100% of any remaining vet costs until the policy renews, and any unused coverage does not roll over to the next year.

Most insurers do not allow you to increase your limit after a diagnosis, and even at renewal, existing conditions can limit coverage changes.

Switching providers can also be risky because pre-existing conditions carry over and new waiting periods may apply.

A $10,000 annual limit is usually enough for most pets, while higher-risk or older pets often need $15,000 or more to avoid running out of coverage during serious treatments.